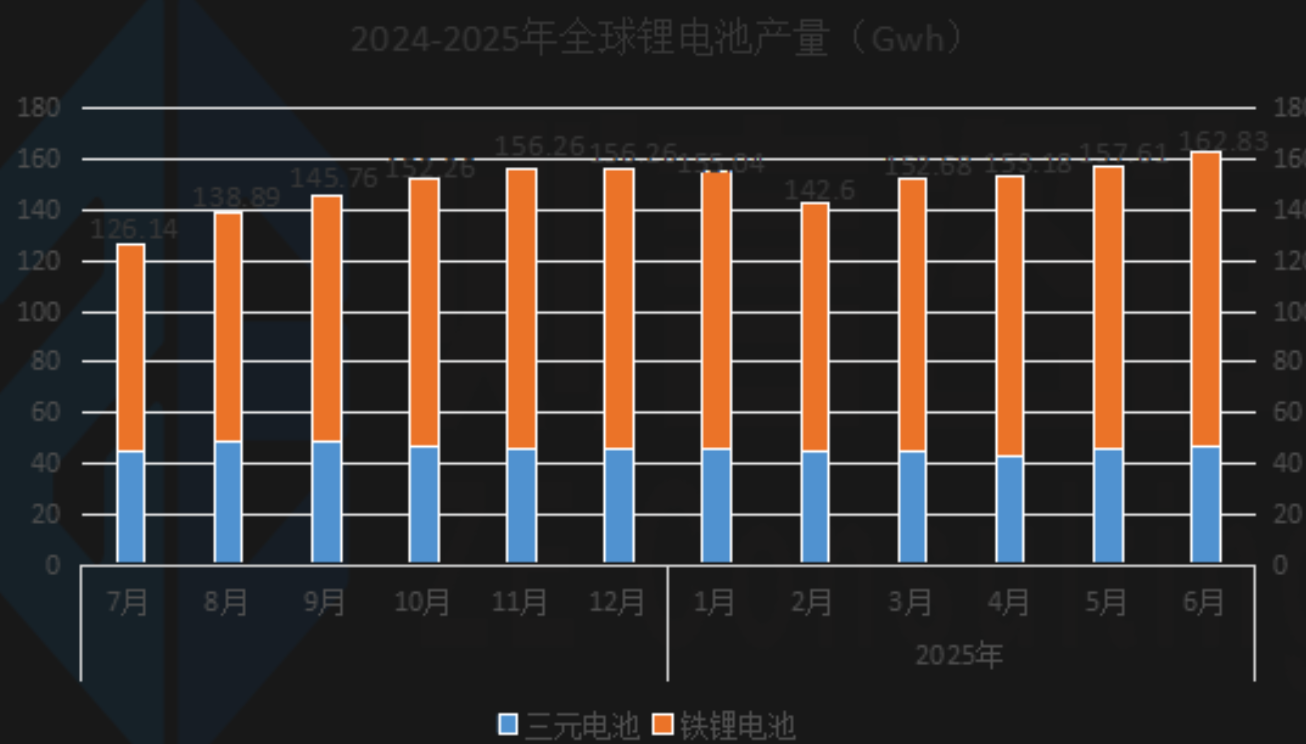

In the first half of 2025, the global lithium battery production reached 923.94 GWh, representing a year-on-year increase of 39.93% and a sequential growth of 5.52% compared to the second half of 2024. Among them:

The production of ternary batteries stood at 271.3 GWh, with a modest year-on-year increase of 1.42%.

The production of lithium iron phosphate (LFP) batteries reached 652.64 GWh, surging by 66.16% year-on-year, becoming the primary driver of overall output growth.

Dominant Players: The "duopoly" pattern of Companies C and B remains solid, with their combined market share exceeding 50%.

Domestic Second-Tier Enterprises: A stable second echelon has formed among Chinese companies, including EVE Energy, Gotion High-Tech, CALB, Xiamen Haichen, Rupow Energy, and Sunwoda. Their total market share exceeds 20%.

Foreign Players: Overseas enterprises, mainly LG Chem, Panasonic, Samsung SDI, and SK On, continued to see their market share decline in the first half of the year, with their combined share dropping to approximately 11%.

So far, the market share of the top 12 battery enterprises has approached 85%, indicating a high level of industry concentration.

subscribe to us

subscribe to us